In the modern world, the race for technological supremacy is increasingly defined not just by innovation, but by access to critical minerals. Rare earth elements (REEs)—essential components in smartphones, electric vehicles, wind turbines, and defense systems—have become one of the most strategic resources on the planet. As of 2024, global reserves stand at roughly 110 million metric tons of rare earth oxide (REO), and the distribution of these resources reveals a striking geopolitical landscape.

China’s Commanding Lead

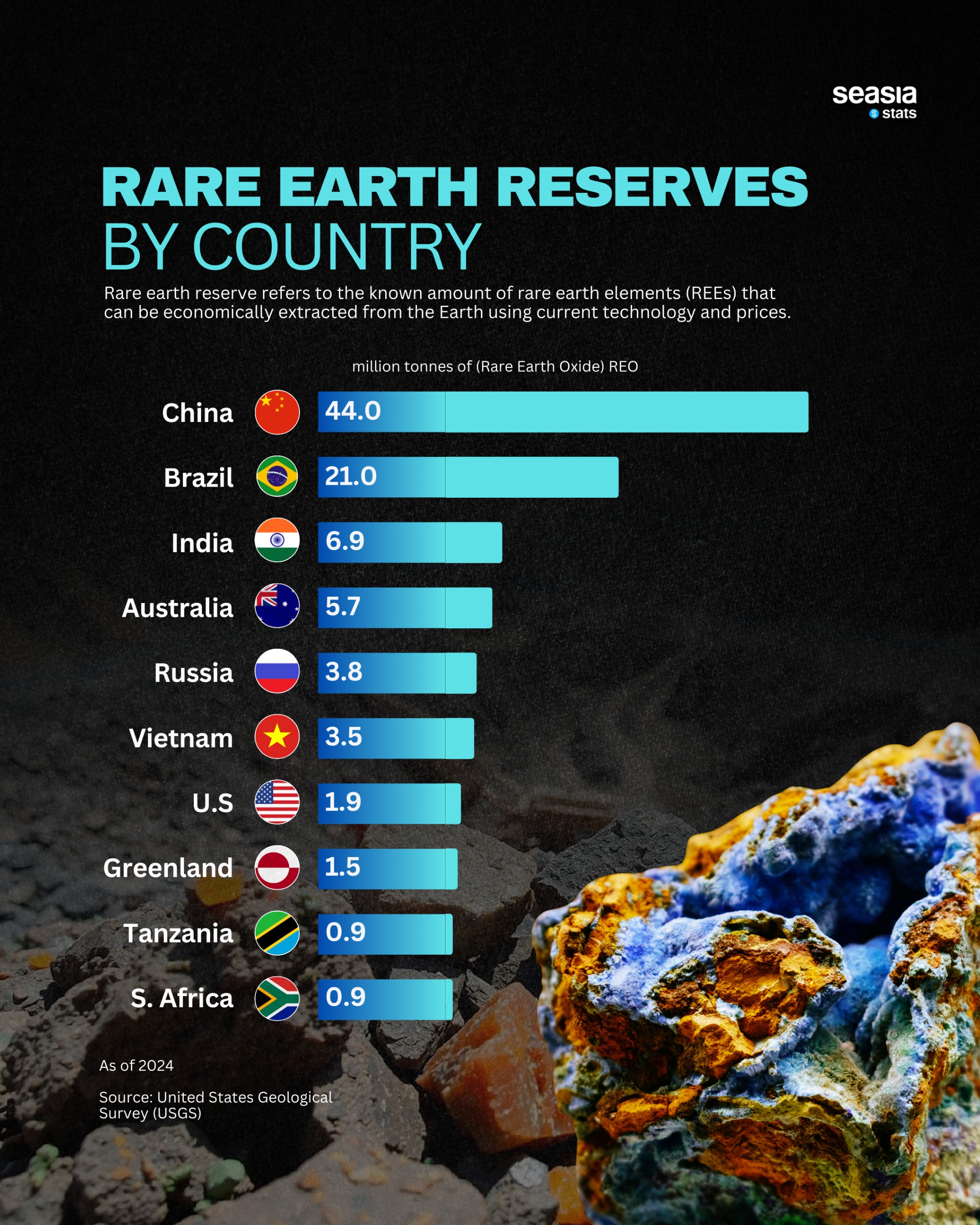

At the center of this landscape stands China, which holds an estimated 44.0 million metric tons of REO—nearly half of the world’s total known reserves. These resources, largely concentrated in bastnäsite deposits and ion-adsorption clays, have given China a dominant role in the global supply chain for advanced electronics, renewable energy technologies, and defense applications.

Beyond reserves, China’s advantage is amplified by its advanced refining capacity and well-established industrial ecosystem. This combination has allowed the country to maintain its position not just as the largest reserve holder, but also as the leading producer and processor of rare earth materials worldwide.

The Rising Tier: Brazil and India

Following China, Brazil holds the second-largest reserves at 21.0 million metric tons—around 23% of the global total. While Brazil’s production levels have historically been modest, new projects such as the Pela Ema deposit are expected to significantly expand output by the late 2020s, positioning the country as a potential alternative supplier.

India ranks third globally with 6.9 million metric tons, primarily located in monazite-rich coastal sands. However, the presence of radioactive thorium has complicated large-scale extraction, slowing development. Still, India’s growing focus on domestic manufacturing and strategic minerals suggests that its rare earth potential could become increasingly important in the coming years.

Key Players Across the Global Map

Other major reserve holders include Australia (5.7 million tons), Russia (3.8 million tons), and Vietnam (3.5 million tons). Australia, in particular, has emerged as a key supplier due to its stable regulatory environment and strong mining sector. Russia and Vietnam also hold significant potential, though development has been uneven due to geopolitical and infrastructural challenges.

The United States, despite being one of the world’s leading producers, has relatively modest reserves of 1.9 million metric tons—just about 2% of the global total. This imbalance has prompted increased investment in recycling technologies and international partnerships to secure long-term supply.

Southeast Asia’s Emerging Role

Southeast Asia is quietly becoming a crucial frontier in the rare earth landscape. Vietnam’s 3.5 million metric tons of reserves make it one of the region’s most important players, with growing interest from international investors seeking to diversify supply chains.

Elsewhere in the region, Malaysia has developed significant processing and refining capabilities, particularly in handling rare earth concentrates from neighboring countries. Indonesia and Thailand are also exploring rare earth potential within broader mineral development strategies, especially as demand for electric vehicles and renewable energy technologies accelerates.

This regional momentum is further supported by ASEAN’s push toward sustainable mining practices and cross-border resource collaboration, positioning Southeast Asia as a key partner in future global supply networks.

Strategic Minerals for a Technological Future

The global distribution of rare earth reserves highlights a fundamental reality: control over these materials is closely tied to economic resilience, technological innovation, and national security. As countries work to reduce reliance on a single dominant supplier, new partnerships, investments, and exploration efforts are reshaping the map of global resource power.

In this evolving landscape, nations with emerging reserves—particularly in Southeast Asia—have a unique opportunity to play a larger role in powering the world’s next generation of technologies.