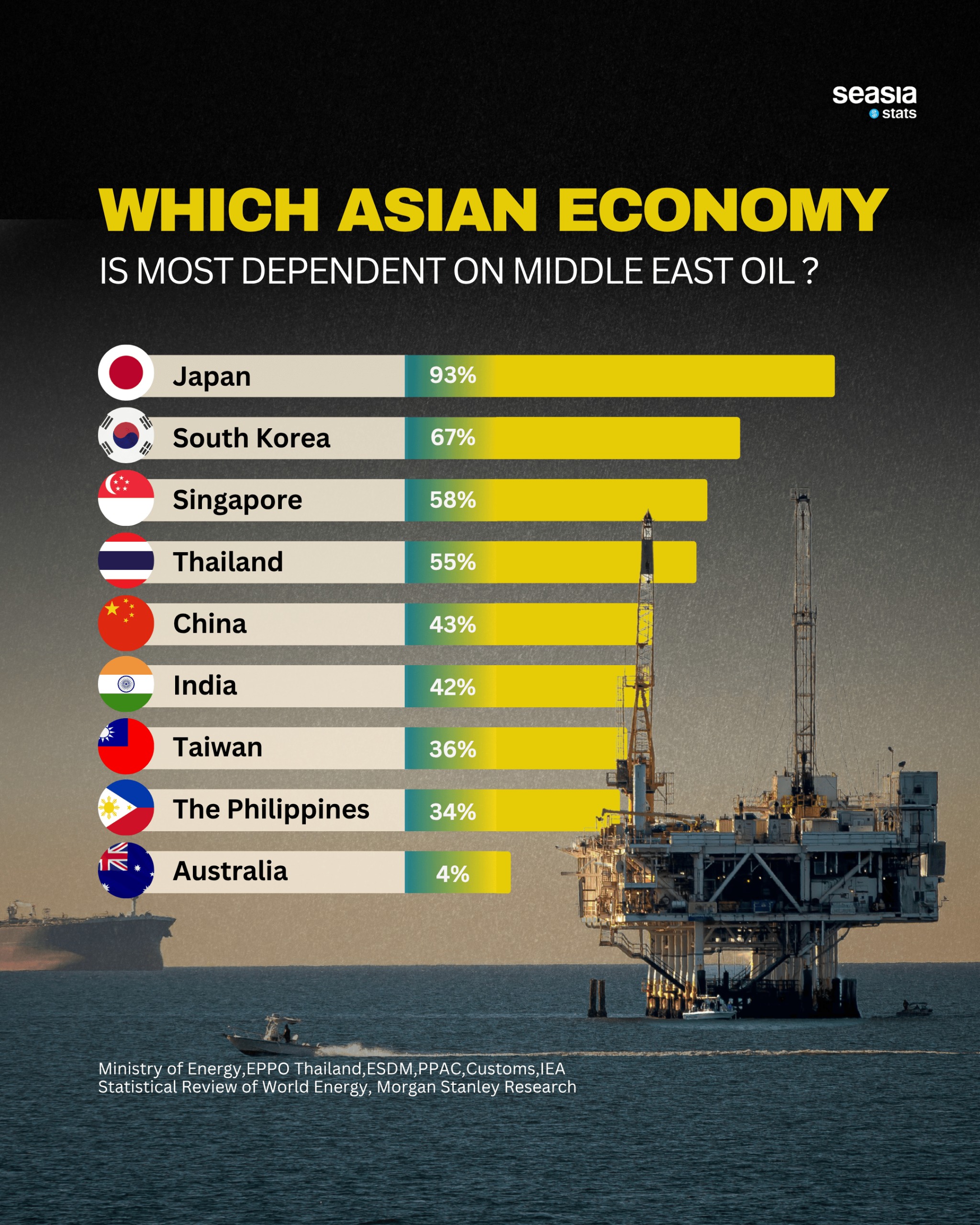

Energy security in Asia has always been shaped by geography, but in today’s uncertain geopolitical climate, it is increasingly defined by dependence. As tensions ripple through the Middle East, a clear reality emerges: many of Asia’s most advanced and fastest-growing economies remain deeply tied to oil flowing from that region.

Japan’s overwhelming reliance

Japan sits at the top of the dependency scale with a striking 93% reliance on Middle Eastern oil. For decades, the country has lacked significant domestic energy resources, forcing it to build one of the most sophisticated import systems in the world. Its refineries, shipping routes, and long-term contracts are all heavily oriented toward suppliers in the Gulf.

This level of dependence is not new, but it has become more precarious in recent years. As Bloomberg once noted, “Japan’s energy security is inseparable from stability in the Middle East,” a reality that leaves the country highly exposed to supply disruptions, price shocks, and geopolitical tensions.

South Korea follows with 67%, reflecting a similar structural vulnerability. Like Japan, it is an industrial powerhouse with limited natural resources, making imported oil essential to sustaining manufacturing, exports, and daily life.

Southeast Asia’s quiet exposure

While Japan and South Korea dominate the headlines, Southeast Asia tells a more complex and increasingly important story. Singapore and Thailand rank third and fourth, with dependency rates of 58% and 55% respectively—figures that underscore how deeply the region is tied to Middle Eastern energy flows.

Singapore’s case is particularly unique. As a global refining and trading hub, it imports crude oil not just for domestic use but for processing and re-export. Its high dependency reflects both consumption and its central role in the global energy supply chain. Stability in the Middle East, therefore, is not just an economic concern for Singapore—it is foundational to its position as an energy hub.

Thailand, meanwhile, represents a broader regional pattern. Despite some domestic production, it relies heavily on imports to meet growing demand from transport, tourism, and industry. This dependency leaves it vulnerable to price volatility, especially during periods of global uncertainty.

The Philippines, with a 34% dependency rate, shows a slightly more diversified sourcing strategy but remains exposed. As an archipelagic nation with rising energy demand, it faces logistical and cost challenges that can amplify global price movements.

Across ASEAN, countries like Indonesia and Malaysia—though not listed in this dataset—illustrate another dimension of the issue. Both are energy producers, yet they still import refined fuel, creating a paradox where resource-rich nations remain sensitive to global oil dynamics.

The balancing act of major economies

China and India, the world’s two most populous nations, sit in the middle of the rankings at 43% and 42%. These figures reflect deliberate diversification strategies. Both countries import from the Middle East but have expanded supply networks to include Russia, Africa, and Latin America.

This diversification provides a buffer, but not immunity. As Reuters has observed, “Asia remains the primary destination for Middle Eastern crude,” meaning that even diversified economies cannot fully escape the region’s influence on global oil markets.

Taiwan, at 36%, mirrors many of these dynamics on a smaller scale, balancing industrial demand with strategic sourcing.

Australia, the outlier—and a glimpse of an alternative

At just 4%, Australia stands apart. Its low dependency highlights the advantage of domestic production and diversified supply chains. While it still participates in global energy markets, it is far less exposed to Middle Eastern disruptions than its Asian neighbors.

This contrast points to a broader question for Asia: how to reduce vulnerability without compromising growth.

A region at an energy crossroads

For Southeast Asia and the wider region, the message is clear. High dependence on Middle Eastern oil is not just an economic statistic—it is a strategic risk. As global tensions persist, countries are accelerating efforts to diversify energy sources, invest in renewables, and build resilience into their systems.

Yet the transition will take time. For now, Asia’s economic engines—from Tokyo to Bangkok to Singapore—remain closely tied to the stability of a region thousands of kilometers away.